Does Homeowners Insurance Cover HVAC?

Search

Recent Posts

Furnace Not Heating? Try These 7 Fixes Before You Call

August 4, 2026

Leaky Ducts: How to Detect and Fix Them

July 30, 2026

Tags

Follow Us on

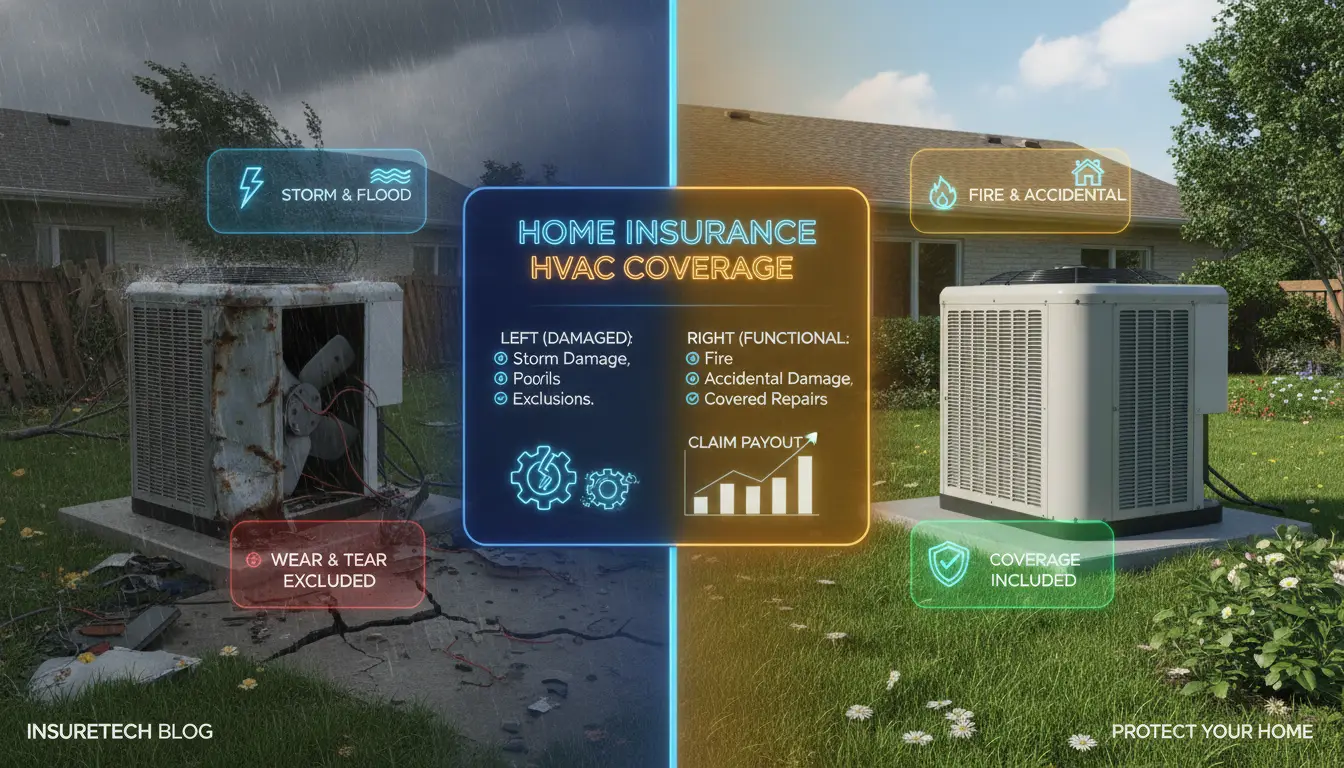

Homeowners insurance covers HVAC damage only when a sudden, unexpected event causes it such as a fire, lightning strike, windstorm, or vandalism. It does not cover normal wear and tear, mechanical breakdown, or lack of maintenance. The type and cause of damage determine whether your policy pays out.

| KEY TAKEAWAYS |

| • Insurance covers HVAC damage from sudden events (fire, lightning, storms, vandalism) but excludes gradual wear, rust, and mechanical failure. |

| • Your HVAC system likely falls under dwelling coverage, not personal property this affects how much you receive if you file a claim. |

| • Actual Cash Value (ACV) policies subtract depreciation, so a 10-year-old unit may yield far less than replacement cost. |

| • Equipment Breakdown Coverage is a low-cost rider that fills the gap standard policies leave for mechanical failure. |

| • Louisiana homeowners face unique risks: hurricane deductibles and the need for separate flood insurance both affect HVAC claim outcomes. |

Your HVAC system just failed, and now you’re staring at a repair estimate that could run into thousands of dollars. Before you open your wallet, you deserve a straight answer about what your homeowners policy will and won’t pay for.

Homeowners insurance can feel like a maze of exceptions and fine print. Many Lafayette Parish residents assume their policy covers everything inside the home. In reality, coverage hinges on one question: what caused the damage?

This guide breaks down exactly how homeowners insurance treats HVAC systems. You’ll learn which damage scenarios qualify for a payout, how your coverage type affects the check you receive, what Louisiana-specific rules change the equation, and when it makes sense to call an adjuster versus paying out of pocket.

The Short Answer- When HVAC Is and Isn’t Covered

When Does Homeowners Insurance Cover HVAC Damage?

Homeowners insurance covers HVAC damage when a named peril causes a sudden, accidental loss. Named perils are the specific events your policy lists as covered causes of damage. Most standard HO-3 policies cover fire, lightning, windstorm, hail, explosion, theft, vandalism, and sudden accidental discharge of water.

If a lightning bolt fries the compressor on your central air unit, that qualifies. If a falling tree branch crushes the outdoor condenser during a storm, that qualifies too. The damage must be sudden and caused by a covered event.

Louisiana homeowners generally carry HO-3 open-peril policies for the dwelling itself, which means all causes of damage are covered unless the policy specifically excludes them.

When Does Homeowners Insurance Not Cover HVAC?

Insurance does not cover HVAC damage from wear and tear, gradual deterioration, or mechanical breakdown. If your 12-year-old air conditioner simply stops cooling because the compressor wore out, your policy will not pay for it.

The same applies to rust, corrosion, mold buildup from poor maintenance, refrigerant leaks that developed slowly, and manufacturer defects. Flood damage is also excluded from standard policies and requires a separate policy through the National Flood Insurance Program (NFIP).

Understanding this distinction upfront saves you from filing a claim that gets denied, which can raise your premiums without any benefit to you.

How Does Homeowners Insurance Classify HVAC Systems?

What Is the Difference Between Dwelling Coverage and Personal Property Coverage?

Dwelling coverage (Coverage A) protects the structure of your home and systems permanently attached to it. Personal property coverage (Coverage C) protects moveable belongings inside your home.

The key difference: dwelling coverage typically pays out at a higher limit, and permanently installed systems receive stronger protection under it.

Which HVAC Systems Fall Under Each Coverage Category?

| HVAC System | Coverage Category | Notes |

| Central air conditioner (split system) | Dwelling (Coverage A) | Permanently installed outdoor unit, air handler, ductwork |

| Furnace or heat pump | Dwelling (Coverage A) | Attached to home structure and ductwork |

| Window AC unit | Personal Property (Coverage C) | Portable, not permanently installed |

| Portable space heater | Personal Property (Coverage C) | Moveable lower coverage limits apply |

| Ductwork | Dwelling (Coverage A) | Built into home structure |

| Mini-split (ductless) | Dwelling (Coverage A) | Wall-mounted unit considered permanently installed |

Why Does HVAC Classification Affect Your Claim Payout?

Dwelling coverage limits are much higher than personal property limits on most policies. A central AC system damaged by a storm would receive a larger payout than a window unit with the same damage, simply because of how each is classified.

Classification also affects whether replacement cost value or actual cash value applies, which we cover in detail below.

What Types of HVAC Damage Are Covered?

Does Homeowners Insurance Cover Fire and Smoke Damage to HVAC?

Fire and smoke damage to your HVAC system is covered under virtually every standard homeowners policy. If a kitchen fire spreads and damages your air handler or furnace, your insurer will pay to repair or replace it.

Smoke damage matters too. Heavy smoke can coat coils, clog filters, and contaminate ductwork to the point where the system requires professional cleaning or replacement. Document all smoke damage with photos before any cleanup.

Does Homeowners Insurance Cover Lightning and Electrical Surge Damage?

Lightning strikes and the electrical surges they cause are covered by named perils. In South Louisiana, where thunderstorms are frequent and powerful, this is one of the most common HVAC insurance claims we see.

A direct lightning strike can destroy a compressor, control board, or capacitor instantly. According to the Insurance Information Institute , lightning damage accounts for a significant share of homeowners property claims each year. Keep your electrical panel surge protection up to date to reduce the risk.

Does Insurance Cover Wind, Hail, and Falling Debris Damage?

Wind, hail, and falling debris are covered perils on most standard policies. A falling tree limb that crushes your outdoor condenser is a straightforward covered claim. Hail dents on coil fins that reduce efficiency are also covered.

However, Louisiana homeowners need to pay attention to separate hurricane or windstorm deductibles, which apply when a named storm causes the damage. This is explained in the Louisiana-specific section below.

Does Insurance Cover Vandalism, Theft, and Sudden Accidental Water Damage?

Vandalism, theft of HVAC components, and sudden accidental water damage are covered. Copper refrigerant line theft is a real problem across South Louisiana if thieves strip your outdoor unit, file a claim.

Sudden accidental water damage, such as a burst pipe that floods your air handler closet, is also covered. The word “sudden” is doing heavy lifting here. A slow leak that rusts out your air handler over months is not covered.

What HVAC Damage Is Not Covered?

Does Insurance Cover Wear and Tear or Mechanical Failure?

No. Wear and tear and mechanical failure are specifically excluded from standard homeowners insurance. This is the most common reason HVAC claims are denied.

If your compressor burns out after years of use, your capacitor fails gradually, or your furnace stops igniting because the igniter wore out, none of these are insurable events. They are the expected costs of owning a mechanical system. This is exactly why equipment breakdown coverage exists, and we cover that option below.

Does Insurance Cover Lack of Maintenance, Rust, and Corrosion?

Policies exclude damage from neglected maintenance, rust, and corrosion. Insurers can and do investigate whether deferred maintenance contributed to a loss.

For example, if your evaporator coil developed a refrigerant leak because the coil corroded over several years, your insurer may deny the claim entirely or reduce the payout because maintenance neglect played a role. Annual HVAC tune-ups create a paper trail that proves you maintained the system.

Scheduling regular maintenance with Fontenot Air Conditioning & Heating not only keeps your system running well, it protects your claim eligibility if something covered does happen.

Does Insurance Cover Manufacturer Defects and Pest Damage?

Manufacturer defects are not covered by homeowners insurance. If a defective part fails prematurely, pursue a warranty claim with the manufacturer instead.

Pest damage, such as mice chewing through wiring or insects nesting in your outdoor unit, is also excluded. Most policies treat pest damage as a maintenance issue the homeowner should prevent.

Does Insurance Cover Flood and Earthquake Damage to HVAC?

Standard homeowners insurance excludes flood and earthquake damage entirely. If floodwater from Hurricane damage or rising bayou water destroys your air handler, your homeowners policy will not pay for it.

You need a separate flood insurance policy through the NFIP or a private flood insurer. Given Lafayette Parish’s flood history, this is not optional coverage. Visit FloodSmart.gov for NFIP policy information.

Does Homeowners Insurance Cover HVAC Repairs and Replacement?

What Repair and Replacement Scenarios Are Covered?

When a covered peril causes HVAC damage, your policy pays for both repair and full replacement if necessary. The insurer does not get to dictate which option their obligation is to restore the system to its pre-loss condition.

Covered scenarios include: replacing a compressor destroyed by lightning, repairing ductwork damaged by a storm, replacing an air handler burned in a fire, and replacing a condenser unit crushed by a falling tree.

What Repair and Replacement Scenarios Are Excluded?

Replacing a failed compressor due to old age, repairing a heat exchanger cracked from years of thermal cycling, fixing a refrigerant leak that developed slowly, and replacing a furnace that simply stopped working are all excluded. The cause must be a sudden covered event, not time or use.

How Do Deductibles Affect What You Actually Receive?

Your deductible is the amount you pay out of pocket before insurance covers the rest. If your deductible is $2,500 and the covered damage totals $3,000, you receive only $500 from your insurer.

For minor HVAC repairs, the deductible can easily exceed the repair cost. In those cases, paying out of pocket is smarter than filing a claim that raises your premiums. A good rule: only file if the covered damage clearly exceeds your deductible by a meaningful margin.

Actual Cash Value vs. Replacement Cost Coverage

How Does Each Coverage Type Pay Out for HVAC Damage?

| Coverage Type | How It Pays | Best For |

| Actual Cash Value (ACV) | Pays depreciated value of damaged system | Lower-premium policies; older systems |

| Replacement Cost Value (RCV) | Pays full cost to replace with like-kind equipment | Newer systems; homeowners wanting full protection |

Actual Cash Value (ACV): ACV pays what your system was worth at the time of the loss, not what it costs to replace it. An 8-year-old AC unit loses significant value each year.

Replacement Cost Value (RCV): RCV pays what it actually costs to buy and install a comparable new unit today. RCV policies cost more in premiums but deliver a much better outcome when you file a claim.

How Does Depreciation Reduce Your HVAC Insurance Payout?

Depreciation is the reduction in value assigned to a system based on age and expected useful life. A central AC system has a typical lifespan of 15 to 20 years. If yours is 10 years old, an ACV policy might assign it 50 to 60 percent depreciation.

That means a $6,000 replacement might yield only $2,400 to $3,000 from an ACV policy after the deductible. The remaining gap comes from your own pocket.

Which Coverage Is Worth Carrying for HVAC Protection?

Replacement Cost Value coverage is worth the additional premium for any HVAC system installed within the last 10 years. If your system is older, weigh the premium difference against the depreciated payout you’d actually receive before deciding.

Ask your insurance agent specifically whether your HVAC system is covered under ACV or RCV. Many homeowners assume RCV but are actually on ACV without realizing it.

Equipment Breakdown Coverage and Home Warranties

What Does Equipment Breakdown Coverage Add to a Standard Policy?

Equipment Breakdown Coverage is an endorsement you add to your homeowners policy that covers sudden mechanical or electrical failure of covered systems. It fills the largest gap in standard coverage: mechanical breakdown from internal causes.

This means if your compressor fails due to an internal electrical fault not old age, not a storm, just an internal breakdown equipment breakdown coverage pays for the repair or replacement. According to the Insurance Information Institute, this endorsement typically costs $25 to $50 per year and covers multiple household systems.

How Does Equipment Breakdown Coverage Differ From a Home Warranty?

| Factor | Equipment Breakdown Coverage | Home Warranty |

| Cost | ~$25–$50/year added to policy | $400–$700/year separate contract |

| Claims process | Through your insurer | Through warranty company (often slower) |

| Coverage trigger | Sudden mechanical/electrical failure | Mechanical failure from normal use |

| Exclusions | Wear and tear still excluded | Pre-existing conditions, maintenance issues |

| HVAC coverage | Yes, including compressor failure | Yes, with service fee per call |

Home warranties can make sense for older systems with higher failure risk. Equipment breakdown coverage is generally the better value for newer systems because of the lower annual cost and faster claims process.

When Does Adding Extra HVAC Coverage Make Financial Sense?

Adding equipment breakdown coverage makes sense if your HVAC system is less than 10 years old, you want protection against internal failures beyond what your homeowners policy covers, and the annual premium is less than 5 percent of what a compressor replacement would cost.

For most Lafayette and Broussard homeowners running central air systems priced at $5,000 to $10,000 to replace, the math clearly favors adding this coverage.

Filing an HVAC Insurance Claim

When Does Filing a Claim Make Sense vs. Paying Out of Pocket?

File a claim when the covered damage clearly exceeds your deductible and the repair or replacement cost is significant. As a general guideline, if the damage total is less than twice your deductible, consider paying out of pocket to avoid a claim on your record.

Claims history affects your premiums. One large, legitimate claim is far better for your long-term rates than two or three small claims in a short period.

How Do You File an HVAC Insurance Claim? Step-by-Step

- Document everything immediately. Take photos and video of the damage from multiple angles before touching anything.

- Prevent further damage. You have a duty to mitigate losses. Cover exposed units, disconnect power if safe, and prevent water intrusion.

- Call your insurance company. Report the claim as soon as possible. Most policies require prompt notification.

- Get a professional assessment. Contact a licensed HVAC contractor to provide a written damage estimate. Fontenot’s AC installation and service team provides written assessments that support the claims process.

- Meet with the adjuster. Walk the adjuster through the damage using your documentation and the contractor’s estimate.

- Review the settlement offer. Compare it to your contractor’s estimate. If the gap is large, ask for a re-evaluation or consult a public adjuster.

How Do You Work With an Insurance Adjuster on an HVAC Claim?

Be prepared and organized. An adjuster’s job is to verify that the damage was caused by a covered peril and to determine a fair payout. Your job is to make that as easy as possible.

Bring your damage photos, your HVAC contractor’s written estimate, any maintenance records you have, and documentation of the weather event if applicable (local weather reports, news coverage). Adjusters respond well to organized, documented claims.

What Are Common Reasons HVAC Claims Are Denied?

- Pre-existing condition: Adjuster determines damage predates the claimed event.

- Excluded peril: Damage caused by flood, wear, or a non-covered event.

- Maintenance neglect: Evidence that deferred maintenance contributed to the loss.

- Late notification: Failing to report promptly as required by your policy.

- Insufficient documentation: No photos, no contractor estimate, no weather records.

Avoiding these five issues eliminates the most common denial triggers before you even file.

HVAC Insurance Considerations for Louisiana Homeowners

How Does Hurricane and Windstorm Damage Affect HVAC Claims in Louisiana?

Wind and hail from hurricanes and tropical storms are covered perils, but Louisiana homeowners face a separate hurricane deductible. This deductible is much higher than the standard deductible and applies specifically when a named storm causes the damage.

After Hurricane Ida in 2021, many Louisiana homeowners discovered that their hurricane deductible was 2 to 5 percent of their home’s insured value, which easily reached $5,000 to $15,000 on a $300,000 home. This can wipe out most or all of an HVAC claim.

Does Standard Insurance Cover Flood Damage to HVAC in Louisiana?

No. Standard homeowners insurance never covers flood damage. In Louisiana, where flood risk is very real from hurricanes, storm surge, and heavy rainfall, a separate flood insurance policy is essential.

The NFIP covers building property including HVAC systems as part of the structure. Coverage limits under the NFIP are capped at $250,000 for the building. If you are in a high-risk flood zone in Lafayette Parish, flood insurance is required by your mortgage lender. Visit FloodSmart.gov to check your flood zone and compare policies.

How Do Louisiana Hurricane Deductibles Work?

Hurricane deductibles are percentage-based, not a flat dollar amount. They apply when a named hurricane, tropical storm, or windstorm (depending on your policy’s trigger language) causes the damage.

For example, a policy with a 3% hurricane deductible on a home insured for $350,000 means you pay the first $10,500 before coverage begins. This is critical to understand when evaluating whether to file an HVAC claim after a storm.

Louisiana’s Department of Insurance provides guidance on hurricane deductible rules for state policies. Review your declarations page or consult your agent to find your specific trigger and percentage. See also Louisiana Department of Insurance consumer resources.

What HVAC Risks Are Specific to Lafayette and Broussard Homeowners?

Homeowners in Lafayette, Broussard, Scott, Youngsville, Carencro, Maurice, and Milton face several HVAC-specific risks that affect both system health and insurance outcomes.

- High humidity accelerates coil corrosion and mold growth inside air handlers, which insurers classify as maintenance issues rather than covered events.

- Storm surge and flash flooding from heavy rainfall can submerge outdoor condenser units, but this damage falls under flood coverage, not homeowners.

- Frequent lightning storms during summer thunderstorm season create real surge risk for compressors and control boards.

- Heat and humidity stress compressors harder than in cooler climates, shortening useful life and increasing mechanical breakdown risk.

Understanding these local risks helps you choose the right coverage combination: a strong homeowners policy, a flood policy, and equipment breakdown coverage.

Conclusion

Homeowners insurance covers HVAC damage from sudden covered events fires, lightning, storms, and vandalism. It does not cover gradual wear, mechanical failure, rust, or flood damage. Whether you receive full replacement cost or a depreciated payout depends entirely on the type of coverage you carry.

For Louisiana homeowners, the stakes are higher. Hurricane deductibles can make storm-related claims far less valuable than expected, and flood damage requires a separate policy entirely. Reviewing your coverage before a storm season starts is far better than discovering gaps after the damage is done. At Fontenot Air Conditioning & Heating, we have helped hundreds of Lafayette Parish homeowners navigate HVAC damage from storms, lightning, and fire. We know what adjusters look for, and we provide written assessments that support your claim.

If your HVAC system has been damaged and you’re not sure whether your policy covers it, contact us. We will assess the system, document the damage professionally, and help you understand your next steps. Reach the Fontenot’s team here we serve Lafayette, Broussard, Scott, Youngsville, Carencro, Maurice, and Milton.

Frequently Asked Questions

Can I file a homeowners insurance claim for a broken AC compressor?

Only if a covered peril caused the failure. A compressor destroyed by a lightning strike or fire is covered. A compressor that failed from age or mechanical wear is not. Your adjuster will investigate the cause, so having a licensed HVAC contractor document the damage strengthens your case.

Does homeowners insurance cover HVAC replacement after a hurricane in Louisiana?

Wind damage from a named storm is covered, but your hurricane deductible applies first. This deductible is typically 2 to 5 percent of your home’s insured value. If the deductible exceeds the HVAC replacement cost, you will pay the full amount out of pocket. Flood damage from storm surge requires a separate NFIP policy.

Is it worth adding equipment breakdown coverage to my homeowners policy?

For most homeowners, yes. Equipment breakdown coverage costs $25 to $50 per year and covers sudden mechanical or electrical failure that standard homeowners insurance excludes. Given that a compressor replacement can cost $1,500 to $3,000 or more in the Lafayette area, the annual premium is a strong value.

Will filing an HVAC insurance claim raise my premiums?

Filing any claim can affect your premiums at renewal, depending on your insurer and your prior claim history. For minor repairs close to your deductible, paying out of pocket is often smarter. Reserve claims for significant covered losses where the payout clearly justifies the potential premium impact.

What documentation do I need to support an HVAC insurance claim?

You need photos and video of the damage taken immediately after the event, a written repair or replacement estimate from a licensed HVAC contractor, documentation of the cause (weather service reports, news coverage for storms), and any prior maintenance records that show you maintained the system properly.

Does homeowners insurance cover ductwork damage?

Yes, ductwork is part of your home’s structure and falls under dwelling coverage. If a covered peril such as a storm, fire, or lightning strike damages your ductwork, your policy covers repair or replacement. Ductwork damaged by pests, moisture, or gradual deterioration is not covered.

Related Articles

Furnace Not Heating? Try These 7 Fixes Before You Call

August 4, 2026